Will Using the 50/30/20 Budget Rule Improve Your Finances?

Will Using the 50/30/20 Budget Rule Improve Your Finances?

Will Using the 50/30/20 Budget Rule Improve Your Finances?

Jul 18, 2019

Budgeting >

Budgeting >

Advanced Concepts

Advanced Concepts

When it comes to budgeting, there's no one size fits all solution.

Personal finance is personal after all; we all have different incomes, desires, attitudes, and approaches to how we handle our finances and pursue our financial goals.

If you're the kind of person who prefers a relaxed, somewhat hands-off approach to budgeting, the 50/30/20 rule may be a good fit for you.

What is the 50/30/20 Budget Method?

The 50/30/20 budget rule is a percentage-based budget method popularized by Senator Elizabeth Warren in her book All Your Worth.

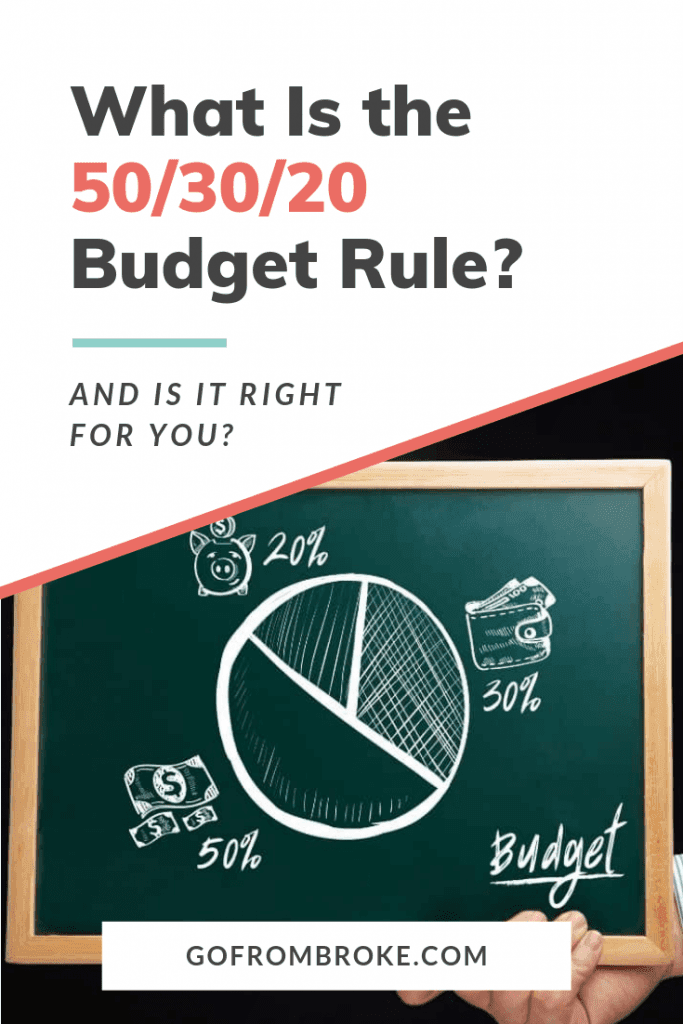

The idea is to divvy up your monthly after-tax income (ie. your take-home pay) across three categories: 50% towards essential expenses, 30% towards discretionary spending, and 20% towards savings and debt repayment.

The 50/30/20 rule's focus on needs, wants, and savings make it a somewhat more relaxed budgeting rule.

This budget method may be perfect for those who want to focus on their savings goals, paying off debt faster, and having more control over their financial lives without the restriction or complexity of a more traditional budget or zero-based budget.

How Does the 50/30/20 Rule Work?

The 50/30/20 rule aims to simplify the budgeting process by breaking it down into just three categories:

Spend 50% of your money on Must-Haves

Use 30% of your money toward Wants

Put 20% of your money toward Savings

Step #1 - Define Your Must-Have Expenses

The general rule of thumb is any expense that has a massive impact on your quality of life is a need or Must-Have.

Must-haves are things you consider non-negotiable for your standard of living.

Your bare-bones living expenses include any fixed expenses like your mortgage or rent payment, car insurance, and health insurance.

They also include any minimum debt payments you have on outstanding obligations like student loans and credit card debt.

According to the 50/30/20 method of budgeting you want your Must-Haves to take up no more than 50% of your after-tax income (your take-home pay).

If you're spending more than 50 percent of your monthly income on your necessities consider downsizing to bring that number back inbounds.

Step #2 - Clarify What You Want

While the 50/30/20 budget method allows you more flexibility with your Wants spending (as long as it falls into the guidelines), it's still important to determine your priorities and evaluate your spending habits to avoid overspending.

Because you won't necessarily have a pre-defined purpose for all of the dollars in your Wants category, it's important to make sure you're spending falls in line with your financial goals.

Just because you can spend 30 percent of your disposable income on eating out, doesn't mean you should.

You'll have a better chance at success if you add a little balance into this segment of your budget.

Also, before you go crazy planning to buy all the things, remember how strict the Must-Haves segment of your budget is.

Things like Netflix, an unlimited cell phone plan, and the bulk of your clothing fall into the Wants category, not under your Needs.

Step #3 - Save for the Future

The final 20% of your money should go toward your Savings goals.

This includes your emergency savings, investments, and any extra payments toward debt beyond the minimum amount due.

It also includes any post-tax retirement contributions you may make, like an investment account or a Roth IRA (Individual Retirement Account).

Even if you have debt, it's a good rule of thumb to use your savings to build up an emergency fund first.

Save an amount large enough to cover unexpected expenses that might cause you to pull out your credit card ($1000 seems to be the standard recommendation by financial experts).

Once you've got your emergency fund filled, throw everything else at your debt payments.

Also, remember that your budget and the percentage allocations are based on your take-home income.

So while you should be funneling everything you can from this 20% segment into your savings account and paying off credit card debt, you should still be contributing to your retirement savings from your pre-tax dollars (via your 401k or a standard IRA).

PRO TIP

Talk to your employer to see if they offer a contribution match. If they do, make sure you're saving at least that much. It's literally free money.

PRO TIP

50-30-20 Budget Example

Let's see what the 50/30/20 monthly budget method looks like in action using a take-home pay of $3,000 a month as an example.

Under the 50/30/20 rule, you'll have $1,500 per month available for your essential monthly expenses (Must-Haves).

Your largest expense is likely to be your housing costs, but keep in mind it isn't your only necessary expense.

If you have a mortgage of $1000, that leaves you with $500 for groceries, a car payment, insurance, utilities, and any minimum payment on your credit cards and student loan debt.

It's entirely possible your housing alone is more than 50% of your take-home pay.

If that's the case, you'll need to make some tough decisions on how to bring your costs down.

The fastest way to reduce your housing expenses is to relocate somewhere cheaper, but that's not always possible.

So here are some other things you can do to reduce your Must-Have expenses:

Try meal planning to reduce your grocery costs

Comparison shop insurance companies

See if your utility providers offer budget billing

Consolidate your debt onto a low-interest credit card with a lower monthly minimum payment

Let's assume for our example, we've got our needs covered with 50% of our income.

Now we're left with $900 for Wants.

Remember, this category includes things like entertainment, your cable bill, clothing, makeup and haircare, gym memberships, etc.

The best way to prevent overspending and stay under the 30% threshold is to stop using credit cards and only spend the cash you have available.

Also, if you have non-negotiable personal expenses that don't fall under Must-Haves, make sure you're paying them first or setting money aside for those bills.

Use my monthly bills calendar to make sure you don't spend all your Wants money before you cover your bills.

Finally, add the remaining $600 to Savings.

Build your emergency fund savings account then put any extra money toward debt payoff and your long-term financial goals.

Problems With the 50/30/20 Rule

The main problem with this budgeting system is that, by itself, it doesn't lend itself to future planning or being intentional with your money.

The 50/30/20 rule accounts for only three major categories, so unless you break down the percentage categories into a more traditional budget structure with more defined budget categories for your spending and sinking funds, you'll likely end up raiding your emergency fund or pulling out the credit card for infrequent and unexpected expenses (like Christmas and insurance premiums).

And by following the general outline, that's exactly what they'll get.

But without breaking down your spending goals further, this budget method isn't really conducive to planning for the future.

Also, actually determining what constitutes a Need, Want, and even Savings can get a bit sticky.

It's all too easy to justify something like your phone bill as a necessity without really examining or reducing the expense.

For those that have struggled with their finances, taking control of your money requires a shift in mindset.

Bottom line: this budget won't provide that.

Who Should Use the 50/30/20 Rule

Do you actively avoid budgeting because it feels too restrictive?

Are you clear on your priorities and rarely feel the urge to spend money on things that aren't part of a greater plan?

Can you stop using credit cards?

If so, then this method may work well for you.

It's also great budgeting method for people who have an aversion to using a budgeting app or a budget spreadsheet since there's no need to monitor or track your spending.

Plus, it offers the flexibility and freedom some people may crave in their budgeting.

Who Should Not Use The 50/30/20 Budget Plan

In a perfect world, this relatively simple approach to budgeting would work for anyone and everyone.

But if you like to know exactly where your money is going, this method may be a little too hands-off for you. You'd be better off using a budget template that breaks down your spending in more detail.

The 50/30/20 budgeting rule is also heavily weighted toward spending.

For those that want to save at a more intense rate, this plan won't get you there.

My Take on the 50/30/20 Budget Rule

For most people, especially those averse to budgeting, I think this method may be a great starting point to improving your financial health.

It's relatively easy to figure out your numbers and divide your income between Must-Haves, Wants, and Savings.

And if you can actually stick to those percentage buckets, you should do ok.

For those struggling to keep your spending under control though, this may not be the plan for you.

The 50/30/20 budget method lacks the awareness and intentionality that you need to really take control of your finances.

Check out The Complete Budget Guide for other options that may suit you better.

When it comes to budgeting, there's no one size fits all solution.

Personal finance is personal after all; we all have different incomes, desires, attitudes, and approaches to how we handle our finances and pursue our financial goals.

If you're the kind of person who prefers a relaxed, somewhat hands-off approach to budgeting, the 50/30/20 rule may be a good fit for you.

What is the 50/30/20 Budget Method?

The 50/30/20 budget rule is a percentage-based budget method popularized by Senator Elizabeth Warren in her book All Your Worth.

The idea is to divvy up your monthly after-tax income (ie. your take-home pay) across three categories: 50% towards essential expenses, 30% towards discretionary spending, and 20% towards savings and debt repayment.

The 50/30/20 rule's focus on needs, wants, and savings make it a somewhat more relaxed budgeting rule.

This budget method may be perfect for those who want to focus on their savings goals, paying off debt faster, and having more control over their financial lives without the restriction or complexity of a more traditional budget or zero-based budget.

How Does the 50/30/20 Rule Work?

The 50/30/20 rule aims to simplify the budgeting process by breaking it down into just three categories:

Spend 50% of your money on Must-Haves

Use 30% of your money toward Wants

Put 20% of your money toward Savings

Step #1 - Define Your Must-Have Expenses

The general rule of thumb is any expense that has a massive impact on your quality of life is a need or Must-Have.

Must-haves are things you consider non-negotiable for your standard of living.

Your bare-bones living expenses include any fixed expenses like your mortgage or rent payment, car insurance, and health insurance.

They also include any minimum debt payments you have on outstanding obligations like student loans and credit card debt.

According to the 50/30/20 method of budgeting you want your Must-Haves to take up no more than 50% of your after-tax income (your take-home pay).

If you're spending more than 50 percent of your monthly income on your necessities consider downsizing to bring that number back inbounds.

Step #2 - Clarify What You Want

While the 50/30/20 budget method allows you more flexibility with your Wants spending (as long as it falls into the guidelines), it's still important to determine your priorities and evaluate your spending habits to avoid overspending.

Because you won't necessarily have a pre-defined purpose for all of the dollars in your Wants category, it's important to make sure you're spending falls in line with your financial goals.

Just because you can spend 30 percent of your disposable income on eating out, doesn't mean you should.

You'll have a better chance at success if you add a little balance into this segment of your budget.

Also, before you go crazy planning to buy all the things, remember how strict the Must-Haves segment of your budget is.

Things like Netflix, an unlimited cell phone plan, and the bulk of your clothing fall into the Wants category, not under your Needs.

Step #3 - Save for the Future

The final 20% of your money should go toward your Savings goals.

This includes your emergency savings, investments, and any extra payments toward debt beyond the minimum amount due.

It also includes any post-tax retirement contributions you may make, like an investment account or a Roth IRA (Individual Retirement Account).

Even if you have debt, it's a good rule of thumb to use your savings to build up an emergency fund first.

Save an amount large enough to cover unexpected expenses that might cause you to pull out your credit card ($1000 seems to be the standard recommendation by financial experts).

Once you've got your emergency fund filled, throw everything else at your debt payments.

Also, remember that your budget and the percentage allocations are based on your take-home income.

So while you should be funneling everything you can from this 20% segment into your savings account and paying off credit card debt, you should still be contributing to your retirement savings from your pre-tax dollars (via your 401k or a standard IRA).

PRO TIP

Talk to your employer to see if they offer a contribution match. If they do, make sure you're saving at least that much. It's literally free money.

PRO TIP

50-30-20 Budget Example

Let's see what the 50/30/20 monthly budget method looks like in action using a take-home pay of $3,000 a month as an example.

Under the 50/30/20 rule, you'll have $1,500 per month available for your essential monthly expenses (Must-Haves).

Your largest expense is likely to be your housing costs, but keep in mind it isn't your only necessary expense.

If you have a mortgage of $1000, that leaves you with $500 for groceries, a car payment, insurance, utilities, and any minimum payment on your credit cards and student loan debt.

It's entirely possible your housing alone is more than 50% of your take-home pay.

If that's the case, you'll need to make some tough decisions on how to bring your costs down.

The fastest way to reduce your housing expenses is to relocate somewhere cheaper, but that's not always possible.

So here are some other things you can do to reduce your Must-Have expenses:

Try meal planning to reduce your grocery costs

Comparison shop insurance companies

See if your utility providers offer budget billing

Consolidate your debt onto a low-interest credit card with a lower monthly minimum payment

Let's assume for our example, we've got our needs covered with 50% of our income.

Now we're left with $900 for Wants.

Remember, this category includes things like entertainment, your cable bill, clothing, makeup and haircare, gym memberships, etc.

The best way to prevent overspending and stay under the 30% threshold is to stop using credit cards and only spend the cash you have available.

Also, if you have non-negotiable personal expenses that don't fall under Must-Haves, make sure you're paying them first or setting money aside for those bills.

Use my monthly bills calendar to make sure you don't spend all your Wants money before you cover your bills.

Finally, add the remaining $600 to Savings.

Build your emergency fund savings account then put any extra money toward debt payoff and your long-term financial goals.

Problems With the 50/30/20 Rule

The main problem with this budgeting system is that, by itself, it doesn't lend itself to future planning or being intentional with your money.

The 50/30/20 rule accounts for only three major categories, so unless you break down the percentage categories into a more traditional budget structure with more defined budget categories for your spending and sinking funds, you'll likely end up raiding your emergency fund or pulling out the credit card for infrequent and unexpected expenses (like Christmas and insurance premiums).

And by following the general outline, that's exactly what they'll get.

But without breaking down your spending goals further, this budget method isn't really conducive to planning for the future.

Also, actually determining what constitutes a Need, Want, and even Savings can get a bit sticky.

It's all too easy to justify something like your phone bill as a necessity without really examining or reducing the expense.

For those that have struggled with their finances, taking control of your money requires a shift in mindset.

Bottom line: this budget won't provide that.

Who Should Use the 50/30/20 Rule

Do you actively avoid budgeting because it feels too restrictive?

Are you clear on your priorities and rarely feel the urge to spend money on things that aren't part of a greater plan?

Can you stop using credit cards?

If so, then this method may work well for you.

It's also great budgeting method for people who have an aversion to using a budgeting app or a budget spreadsheet since there's no need to monitor or track your spending.

Plus, it offers the flexibility and freedom some people may crave in their budgeting.

Who Should Not Use The 50/30/20 Budget Plan

In a perfect world, this relatively simple approach to budgeting would work for anyone and everyone.

But if you like to know exactly where your money is going, this method may be a little too hands-off for you. You'd be better off using a budget template that breaks down your spending in more detail.

The 50/30/20 budgeting rule is also heavily weighted toward spending.

For those that want to save at a more intense rate, this plan won't get you there.

My Take on the 50/30/20 Budget Rule

For most people, especially those averse to budgeting, I think this method may be a great starting point to improving your financial health.

It's relatively easy to figure out your numbers and divide your income between Must-Haves, Wants, and Savings.

And if you can actually stick to those percentage buckets, you should do ok.

For those struggling to keep your spending under control though, this may not be the plan for you.

The 50/30/20 budget method lacks the awareness and intentionality that you need to really take control of your finances.

Check out The Complete Budget Guide for other options that may suit you better.

When it comes to budgeting, there's no one size fits all solution.

Personal finance is personal after all; we all have different incomes, desires, attitudes, and approaches to how we handle our finances and pursue our financial goals.

If you're the kind of person who prefers a relaxed, somewhat hands-off approach to budgeting, the 50/30/20 rule may be a good fit for you.

What is the 50/30/20 Budget Method?

The 50/30/20 budget rule is a percentage-based budget method popularized by Senator Elizabeth Warren in her book All Your Worth.

The idea is to divvy up your monthly after-tax income (ie. your take-home pay) across three categories: 50% towards essential expenses, 30% towards discretionary spending, and 20% towards savings and debt repayment.

The 50/30/20 rule's focus on needs, wants, and savings make it a somewhat more relaxed budgeting rule.

This budget method may be perfect for those who want to focus on their savings goals, paying off debt faster, and having more control over their financial lives without the restriction or complexity of a more traditional budget or zero-based budget.

How Does the 50/30/20 Rule Work?

The 50/30/20 rule aims to simplify the budgeting process by breaking it down into just three categories:

Spend 50% of your money on Must-Haves

Use 30% of your money toward Wants

Put 20% of your money toward Savings

Step #1 - Define Your Must-Have Expenses

The general rule of thumb is any expense that has a massive impact on your quality of life is a need or Must-Have.

Must-haves are things you consider non-negotiable for your standard of living.

Your bare-bones living expenses include any fixed expenses like your mortgage or rent payment, car insurance, and health insurance.

They also include any minimum debt payments you have on outstanding obligations like student loans and credit card debt.

According to the 50/30/20 method of budgeting you want your Must-Haves to take up no more than 50% of your after-tax income (your take-home pay).

If you're spending more than 50 percent of your monthly income on your necessities consider downsizing to bring that number back inbounds.

Step #2 - Clarify What You Want

While the 50/30/20 budget method allows you more flexibility with your Wants spending (as long as it falls into the guidelines), it's still important to determine your priorities and evaluate your spending habits to avoid overspending.

Because you won't necessarily have a pre-defined purpose for all of the dollars in your Wants category, it's important to make sure you're spending falls in line with your financial goals.

Just because you can spend 30 percent of your disposable income on eating out, doesn't mean you should.

You'll have a better chance at success if you add a little balance into this segment of your budget.

Also, before you go crazy planning to buy all the things, remember how strict the Must-Haves segment of your budget is.

Things like Netflix, an unlimited cell phone plan, and the bulk of your clothing fall into the Wants category, not under your Needs.

Step #3 - Save for the Future

The final 20% of your money should go toward your Savings goals.

This includes your emergency savings, investments, and any extra payments toward debt beyond the minimum amount due.

It also includes any post-tax retirement contributions you may make, like an investment account or a Roth IRA (Individual Retirement Account).

Even if you have debt, it's a good rule of thumb to use your savings to build up an emergency fund first.

Save an amount large enough to cover unexpected expenses that might cause you to pull out your credit card ($1000 seems to be the standard recommendation by financial experts).

Once you've got your emergency fund filled, throw everything else at your debt payments.

Also, remember that your budget and the percentage allocations are based on your take-home income.

So while you should be funneling everything you can from this 20% segment into your savings account and paying off credit card debt, you should still be contributing to your retirement savings from your pre-tax dollars (via your 401k or a standard IRA).

PRO TIP

Talk to your employer to see if they offer a contribution match. If they do, make sure you're saving at least that much. It's literally free money.

PRO TIP

50-30-20 Budget Example

Let's see what the 50/30/20 monthly budget method looks like in action using a take-home pay of $3,000 a month as an example.

Under the 50/30/20 rule, you'll have $1,500 per month available for your essential monthly expenses (Must-Haves).

Your largest expense is likely to be your housing costs, but keep in mind it isn't your only necessary expense.

If you have a mortgage of $1000, that leaves you with $500 for groceries, a car payment, insurance, utilities, and any minimum payment on your credit cards and student loan debt.

It's entirely possible your housing alone is more than 50% of your take-home pay.

If that's the case, you'll need to make some tough decisions on how to bring your costs down.

The fastest way to reduce your housing expenses is to relocate somewhere cheaper, but that's not always possible.

So here are some other things you can do to reduce your Must-Have expenses:

Try meal planning to reduce your grocery costs

Comparison shop insurance companies

See if your utility providers offer budget billing

Consolidate your debt onto a low-interest credit card with a lower monthly minimum payment

Let's assume for our example, we've got our needs covered with 50% of our income.

Now we're left with $900 for Wants.

Remember, this category includes things like entertainment, your cable bill, clothing, makeup and haircare, gym memberships, etc.

The best way to prevent overspending and stay under the 30% threshold is to stop using credit cards and only spend the cash you have available.

Also, if you have non-negotiable personal expenses that don't fall under Must-Haves, make sure you're paying them first or setting money aside for those bills.

Use my monthly bills calendar to make sure you don't spend all your Wants money before you cover your bills.

Finally, add the remaining $600 to Savings.

Build your emergency fund savings account then put any extra money toward debt payoff and your long-term financial goals.

Problems With the 50/30/20 Rule

The main problem with this budgeting system is that, by itself, it doesn't lend itself to future planning or being intentional with your money.

The 50/30/20 rule accounts for only three major categories, so unless you break down the percentage categories into a more traditional budget structure with more defined budget categories for your spending and sinking funds, you'll likely end up raiding your emergency fund or pulling out the credit card for infrequent and unexpected expenses (like Christmas and insurance premiums).

And by following the general outline, that's exactly what they'll get.

But without breaking down your spending goals further, this budget method isn't really conducive to planning for the future.

Also, actually determining what constitutes a Need, Want, and even Savings can get a bit sticky.

It's all too easy to justify something like your phone bill as a necessity without really examining or reducing the expense.

For those that have struggled with their finances, taking control of your money requires a shift in mindset.

Bottom line: this budget won't provide that.

Who Should Use the 50/30/20 Rule

Do you actively avoid budgeting because it feels too restrictive?

Are you clear on your priorities and rarely feel the urge to spend money on things that aren't part of a greater plan?

Can you stop using credit cards?

If so, then this method may work well for you.

It's also great budgeting method for people who have an aversion to using a budgeting app or a budget spreadsheet since there's no need to monitor or track your spending.

Plus, it offers the flexibility and freedom some people may crave in their budgeting.

Who Should Not Use The 50/30/20 Budget Plan

In a perfect world, this relatively simple approach to budgeting would work for anyone and everyone.

But if you like to know exactly where your money is going, this method may be a little too hands-off for you. You'd be better off using a budget template that breaks down your spending in more detail.

The 50/30/20 budgeting rule is also heavily weighted toward spending.

For those that want to save at a more intense rate, this plan won't get you there.

My Take on the 50/30/20 Budget Rule

For most people, especially those averse to budgeting, I think this method may be a great starting point to improving your financial health.

It's relatively easy to figure out your numbers and divide your income between Must-Haves, Wants, and Savings.

And if you can actually stick to those percentage buckets, you should do ok.

For those struggling to keep your spending under control though, this may not be the plan for you.

The 50/30/20 budget method lacks the awareness and intentionality that you need to really take control of your finances.

Check out The Complete Budget Guide for other options that may suit you better.

Need some help?

Whether you're struggling to stick to a budget, overwhelmed with debt, or just wanting to feel a bit more in control, I'm happy to guide you toward your best next step.

Need some help?

Whether you're struggling to stick to a budget, overwhelmed with debt, or just wanting to feel a bit more in control, I'm happy to guide you toward your best next step.

Need some help?

Whether you're struggling to stick to a budget, overwhelmed with debt, or just wanting to feel a bit more in control, I'm happy to guide you toward your best next step.

You're in good hands

You're in good hands

You're in good hands

© 2024 GO FROM BROKE

This site may contain affiliate links. As an Amazon Associate, I earn from qualifying purchases. Please read my disclosure policy for more info.

© 2024 GO FROM BROKE

This site may contain affiliate links. As an Amazon Associate, I earn from qualifying purchases. Please read my disclosure policy for more info.

© 2024 GO FROM BROKE

This site may contain affiliate links. As an Amazon Associate, I earn from qualifying purchases. Please read my disclosure policy for more info.